Default Correlation

From Open Risk Manual

Revision as of 15:57, 3 April 2019 by Wiki admin (talk | contribs)

Contents

Definition

Default Correlation denotes a measure of Default Dependency between different borrowers when considered as part of a Credit Portfolio. It measures the likelihood of Joint Default within the period of consideration.

Formula

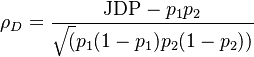

Generic Default Correlation

The general formula for default correlation between two obligors is linking to the Joint Default probability:

where  are is the Probability of Default of each obligor

are is the Probability of Default of each obligor

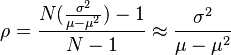

From Default Rate Volatility

Given an estimate  of Default Rate Volatility for a homogeneous credit portfolio, the average default correlation is[1]

of Default Rate Volatility for a homogeneous credit portfolio, the average default correlation is[1]

See Also

References

- ↑ Credit Metrics Technical Document, 1997