Difference between revisions of "Var-Covar Model"

Wiki admin (talk | contribs) |

Wiki admin (talk | contribs) |

||

| Line 20: | Line 20: | ||

* The lack of any fundamental drivers in establishing the dependency / correlation structure limits the usefulness of the approach as a [[Risk Management]] tool | * The lack of any fundamental drivers in establishing the dependency / correlation structure limits the usefulness of the approach as a [[Risk Management]] tool | ||

* Established correlations may be unstable | * Established correlations may be unstable | ||

| − | * Does not capture possible | + | * Does not capture possible [[Tail Risk]] correlations if the dependency structure is assumed Gaussian |

== References == | == References == | ||

Latest revision as of 13:00, 16 April 2021

Contents

Definition

Var-Covar (Variance-Coveriance) model denotes a simple methodology that allows the Risk Aggregation of distinct risk types once their individual risk profile and their dependency have been already modelled.

Methodology

The methodology is based[1] on combining the marginal, standalone distributions of the modelled risk type (PnL, losses etc), into a single aggregate loss distribution. The main requirement for implementing the approach is to characterise the level of interdependence of standalone losses, which is typically accomplished with a matrix of correlations.

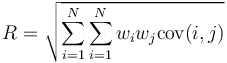

Formula

where R is the aggregated risk, w(i) are the concentration weights of the contributing risk types and cov(i,j) is the covariance between risk types

Usage

Var-Covar can be applied at different levels of risk aggregation, e.g, to aggregate Market Risk in the Trading Book. Another use is to apply Var-Covar at the top level of risk aggregation, for example combining the market, credit and operational risk types for the purposes of the ICAAP process.

Advantages

The main advantage of the Var-Covar model is that it uses a limited number of inputs, can be evaluated very easily, and does not require fundamental information about lower-level risks.

Issues and Challenges

- The lack of any fundamental drivers in establishing the dependency / correlation structure limits the usefulness of the approach as a Risk Management tool

- Established correlations may be unstable

- Does not capture possible Tail Risk correlations if the dependency structure is assumed Gaussian

References

- ↑ BCBS, Developments in Modelling Risk Aggregation, 2010