Default Rate Process

From Open Risk Manual

Revision as of 11:18, 3 April 2019 by Wiki admin (talk | contribs)

Definition

Default Rate Process is any stochastic process that aims to model the arrival of default events in a Credit Portfolio

A default rate process is related to the corresponding Credit Loss Process which incorporates additional Loss Given Default considerations

Formula

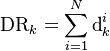

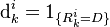

A default rate process is modelled as the cumulation of individual transitions of Credit Rating into the defaulted state. The individual default indicator for an entity  is simply

is simply

where  is the rating state at observation point k

is the rating state at observation point k

The default rate process is the sum (defined on a fixed cohort basis) of individual random variables