Difference between revisions of "Portfolio Stability Index"

From Open Risk Manual

Wiki admin (talk | contribs) |

Wiki admin (talk | contribs) (→Formula) |

||

| (One intermediate revision by the same user not shown) | |||

| Line 7: | Line 7: | ||

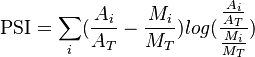

== Formula == | == Formula == | ||

:<math> | :<math> | ||

| − | PSI = \sum_i (\frac{A_i}{A_T} | + | \mbox{PSI} = \sum_i (\frac{A_i}{A_T} - \frac{M_i}{M_T}) log(\frac{\frac{A_i}{A_T}}{\frac{M_i}{M_T}}) |

</math> | </math> | ||

| Line 15: | Line 15: | ||

* <math>M_i</math> is modelled default rate for class i | * <math>M_i</math> is modelled default rate for class i | ||

* <math>A_T, M_T</math> are the total actual and modelled default rates respectively | * <math>A_T, M_T</math> are the total actual and modelled default rates respectively | ||

| − | |||

== See Also == | == See Also == | ||

Latest revision as of 17:32, 17 February 2022

Contents

Definition

Portfolio Stability Index (PSI, more general: Population Stability Index) is a measure of the divergence of frequency distributions between two samples (typically over time)

Usage

The index is used to measure the divergence between a development sample and the current portfolio as part of monitoring or Credit Scorecard Validation.

Formula

where

-

is the i-th Credit Score band

is the i-th Credit Score band -

is actual default rate for class i

is actual default rate for class i -

is modelled default rate for class i

is modelled default rate for class i -

are the total actual and modelled default rates respectively

are the total actual and modelled default rates respectively