Difference between revisions of "PCAF Methodology"

Wiki admin (talk | contribs) (Created page with "== Definition == Any of the PCAF proposed methodologies<ref>PCAF (2020). The Global GHG Accounting and Reporting Standard for the Financial Industry.</ref> == Specific As...") |

Wiki admin (talk | contribs) |

||

| (4 intermediate revisions by the same user not shown) | |||

| Line 1: | Line 1: | ||

== Definition == | == Definition == | ||

| − | + | '''PCAF Methodology''' denotes any of the [[Partnership for Carbon Accounting Financials]] proposed methodologies<ref>PCAF (2020). The Global GHG Accounting and Reporting Standard for the Financial Industry.</ref> for attributing [[GHG Emissions]] to diverse financial contracts. The essence of the methodology is a linear attribution of emissions using measures that capture on the one hand (numerator) a measure of the monetary value of the financial contract and on the other hand (denominator) a measure of the total value of the project, company or asset that is being financed. | |

| + | |||

| + | == Formula == | ||

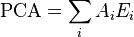

| + | The stylized formula that results from the application of the methodology defines the [[Portfolio Carbon Footprint]] and is given by | ||

| + | |||

| + | :<math> | ||

| + | \mbox{PCA} = \sum_i A_i E_i | ||

| + | </math> | ||

| + | |||

| + | where the index i runs over the components of the portfolio (clients, contracts, etc), A is the attribution factor and E are emissions in suitable units (e.g. CO2 equivalent). The precise definition of A and E depends on | ||

| + | * the specific financial asset class which determines the type of contactual relations and available financial data | ||

| + | * the specific emissions and emissions measurement technologies which determine the available data | ||

== Specific Asset Class Methodologies == | == Specific Asset Class Methodologies == | ||

| Line 6: | Line 17: | ||

* Listed equity and corporate bonds | * Listed equity and corporate bonds | ||

* Business loans and unlisted equity | * Business loans and unlisted equity | ||

| − | * [[PCAF Methodology for Project Finance | Project | + | * [[PCAF Methodology for Project Finance | Project Finance]] |

* Commercial real estate | * Commercial real estate | ||

| − | * Mortgages | + | * [[PCAF Methodology for Mortgages | Mortages]] |

* Motor vehicle loans | * Motor vehicle loans | ||

| + | |||

| + | == References == | ||

| + | <references/> | ||

[[Category:PCAF]] | [[Category:PCAF]] | ||

Latest revision as of 10:34, 11 March 2022

Definition

PCAF Methodology denotes any of the Partnership for Carbon Accounting Financials proposed methodologies[1] for attributing GHG Emissions to diverse financial contracts. The essence of the methodology is a linear attribution of emissions using measures that capture on the one hand (numerator) a measure of the monetary value of the financial contract and on the other hand (denominator) a measure of the total value of the project, company or asset that is being financed.

Formula

The stylized formula that results from the application of the methodology defines the Portfolio Carbon Footprint and is given by

where the index i runs over the components of the portfolio (clients, contracts, etc), A is the attribution factor and E are emissions in suitable units (e.g. CO2 equivalent). The precise definition of A and E depends on

- the specific financial asset class which determines the type of contactual relations and available financial data

- the specific emissions and emissions measurement technologies which determine the available data

Specific Asset Class Methodologies

- Listed equity and corporate bonds

- Business loans and unlisted equity

- Project Finance

- Commercial real estate

- Mortages

- Motor vehicle loans

References

- ↑ PCAF (2020). The Global GHG Accounting and Reporting Standard for the Financial Industry.