Difference between revisions of "Gross Carrying Amount"

From Open Risk Manual

Wiki admin (talk | contribs) |

(No difference)

|

Latest revision as of 13:06, 25 May 2020

Definition

Gross Carrying Amount, in the context of IFRS 9 [1], is the Amortised Cost of a financial asset, before adjusting for any Loss Allowance

Formula

Expressed as a derived measure, the formula for the gross carrying amount simply reflects the fact that it is defined as the amortized cost without the loss allowance deduction

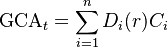

In terms of cashflows, given a set of expected cashflows  (with index running from 1 to n) and a set of discount factors D calculated using the compound Effective Interest Rate over the expected life T of a financial asset, the GCA is obtained as follows:

(with index running from 1 to n) and a set of discount factors D calculated using the compound Effective Interest Rate over the expected life T of a financial asset, the GCA is obtained as follows:

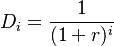

where the discount factor for period (i) is given by

See Also

References

- ↑ IFRS Standard 9, Financial Instruments