Difference between revisions of "Divergence Statistic"

From Open Risk Manual

Wiki admin (talk | contribs) |

Wiki admin (talk | contribs) |

||

| Line 1: | Line 1: | ||

== Definition == | == Definition == | ||

| − | The '''Divergence Statistic''' is a measure of the distance between two distributions. It is typically used in assessing the ability of a [[Credit | + | The '''Divergence Statistic''' is a measure of the distance between two distributions. It is typically used in assessing the ability of a [[Credit Scorecard]] to distinguish between the ''good'' and ''bad'' populations |

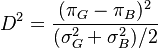

== Formula == | == Formula == | ||

:<math> | :<math> | ||

| − | D^2 = \frac{\pi_G - \pi_B)^2}{(\sigma^2_G + \sigma^2_B)/2} | + | D^2 = \frac{(\pi_G - \pi_B)^2}{(\sigma^2_G + \sigma^2_B)/2} |

</math> | </math> | ||

Latest revision as of 17:29, 17 February 2022

Definition

The Divergence Statistic is a measure of the distance between two distributions. It is typically used in assessing the ability of a Credit Scorecard to distinguish between the good and bad populations