Cumulative Default Probability

From Open Risk Manual

Revision as of 11:23, 31 March 2021 by Wiki admin (talk | contribs)

Definition

The term Cumulative Default Probability is used in the context of multi-period Credit Risk analysis to denote the likelihood that a Legal Entity is observed to have experienced a defined Credit Event up to a particular timepoint.

The cumulative default probability can be considered as the primary representation of the Credit Curve as a set of non-decreasing probabilities

- In terms of the Incremental Default Probability we have

where we denote with

where we denote with  the incremental default probability during time

the incremental default probability during time ![[t_{k-1}, t_k]](https://www.openriskmanual.org/wiki/images/mathdata/5/f/c/5fca5d2a31e321534bcf5a74a56b3db1.png)

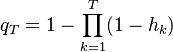

- In terms of the Marginal Default Probability we have

where

where  is the marginal default probability during period . The marginal default probability is also denoted the Hazard Rate

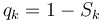

is the marginal default probability during period . The marginal default probability is also denoted the Hazard Rate - In terms of the Survival Probability we have

where

where  is the survival probability up to point

is the survival probability up to point