Rating System Cyclicality

From Open Risk Manual

Revision as of 19:40, 15 October 2017 by Wiki admin (talk | contribs)

Contents

Definition

Rating System Cyclicality refers to characteristics of a Credit Rating System with respect to it dynamic response to evolving economic (and thus credit conditions).

Point in Time System Behaviour

A fully cyclical rating system or ‘Point-in-time’ (PiT) would see an economic downturn picked up through migration of exposures to lower rating grades and therefore no increase in default rate within a grade.

Through the Cycle System Behaviour

At the other extreme a non-cyclical or ‘Through-the-cycle’ (TtC) rating system does not respond to an economic downturn with grade migration, but the default rate within a grade increases instead.

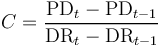

Assessment of Cyclicality

A direct measure of cyclicality in terms of rating system based Probability of Default measures and observed Default Rate is given by[1]

References

- ↑ BOE, Supervisory Statement SS11/13, June 2017