Cumulative Default Rate

From Open Risk Manual

Definition

The term Cumulative Default Rate is used in the context of multi-period credit risk analysis to denote the empirical (or modelled) default rate observed in a certain portfolio as it cumulates (aggregates) up to a final point in time.

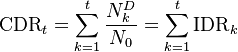

The cumulative default rate up to time period k is denoted  and can be considered as the integral (sum) of the Incremental Default Rate

and can be considered as the integral (sum) of the Incremental Default Rate

Formula

The cumulative default rate during period k, given an initial count of N0 and incremental default rate NtD

See Also

- For the relationship with the Incremental Default Probability, see Probability of Default versus Default Rate