Cohort Estimator

Contents

Definition

The Cohort estimator is a simple frequentist estimation of multi-state transitions. The estimator can be used to derive the transition probability matrix of a Markov process with a finite number of states

Single Period Cohort Estimator

The position in state space for an entity  at discrete time

at discrete time  is a random variable

is a random variable  taking values in the state space S. We assume a finite state space

taking values in the state space S. We assume a finite state space

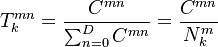

Let  be the number (count) of entities at state m at time k-1 and at state n at k. The directly estimated transition probability is:

be the number (count) of entities at state m at time k-1 and at state n at k. The directly estimated transition probability is:

The estimator reflects that the probability of transition from m to n is the observed count number of all entities that migrated from m to n as a fraction of the count of all entities whose rating was m at k-1, that is,  , irrespective of where they migrated to. The denominator includes all entities that did not migrate

, irrespective of where they migrated to. The denominator includes all entities that did not migrate

State changes which occur within the period [k-1,k] are obviously ignored, so the time resolution must be chosen so that there is as little ignored transition history as possible.

Multi-Period Cohort Estimator

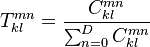

A multi-period estimator without the assumption of time-homogeneity is also straight-forward:

where  denotes the migration count of the period [k,l].

denotes the migration count of the period [k,l].

Confidence Intervals

Confidence intervals for the cohort estimator can be estimated using the multinomial proportions method[1]

Issues and Challenges

- The cohort estimator gives zero probability to a migration event that is not present in the data. E.g. in the presence of (right) censoring where we do not know what happens to the firm after the sample window closes (e.g. does it default right away or does it live on until the present) [2]

- Left truncation where firms only enter sample if they have either survived long enough or have received a rating.